Americans that have had the ability to keep their jobs and still work throughout the coronavirus have been spending significantly less money. This has led to a new record of American’s stockpiling cash and increasing savings, reaching an average of 33% of disposable income being saved in April of this year according to the U.S. Bureau of Economic Analysis. This is the highest this number has been since they started tracking this number in the 1960s. According to FactSet, the second closest record high savings rate was in 1975 at 17.3% in comparison to the 33% in 2020. This savings increase is happening at the same time 40 million Americans have filed for unemployment due to the pandemic. The uncertainty and fear, plus restraints placed by social distancing and the shutdown has decreased the ability and desire to go out and spend money. Gregory Daco, chief U.S. economist at Oxford Economics stated, “There is a tremendous uncertainty and virus fear that is lingering, and that is restraining people’s desire to go out and spend as they normally would.”

The U.S. consumer is responsible for two-thirds of the economy. The economic turnaround and recovery will depend upon why Americans are saving more and if this will be a short-term or long-term effect of the virus. It seems like this increase in savings is a direct result of the business shutdowns. Is the savings fear based? Or is the increase in savings from strategic changes in consumer habits based on a restructuring of how people spend their money? Will these changes in spending last, or will they dissolve as uncertainty disappears and things go back to normal? The average American household has decreased spending by a record of 13.6% per month according to economists. This is mostly due to decreased opportunity to spend money since the places most Americans typically spent money were shut down. But how will this season of forced savings change the future?

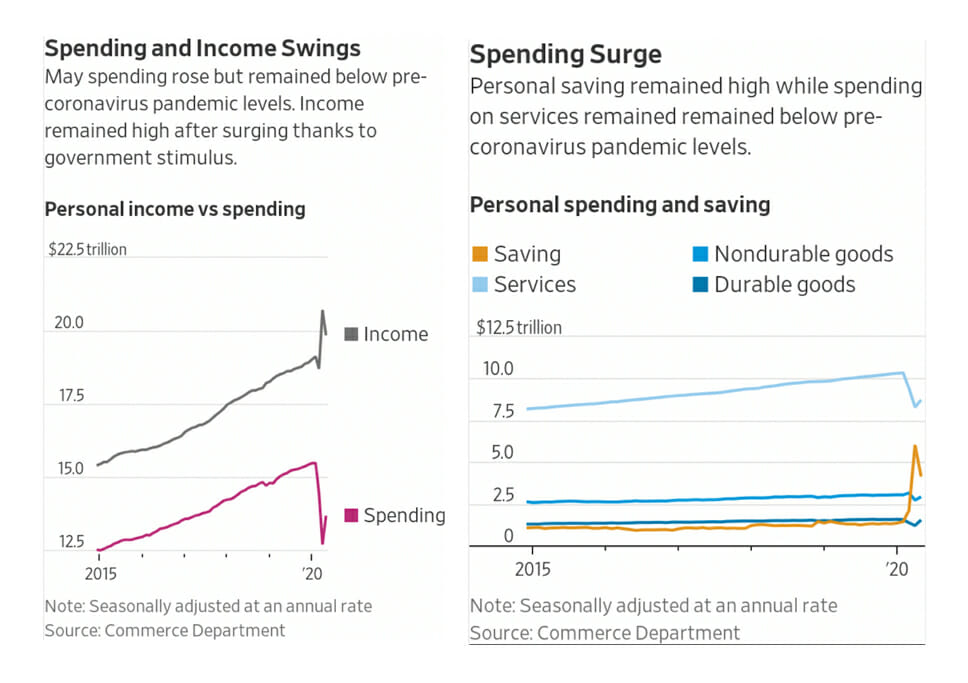

It seems very likely that as soon as shops and restaurants open back up the pendulum will shift back to decreased savings and increased spending. In May, consumer spending in the U.S. rebounded, but according to the Wall Street Journal, the virus surges across the country are posing a second wave of economic threat. After the decrease in spending, May saw a personal consumption increase of 8.2% from the month prior, according to the Commerce Department, showing a record increase in spending. It seems American’s are jumping at the chance to spend money again as the economy opens back up, but we will have to wait and see how it plays out as new waves of the virus cause states to roll back their re-opening. While we wait to see what happens, maybe we should ask ourselves if we can continue to make adjustments to our spending habits even after the pandemic dissipates.

If you are part of this statistic, and you have decreased your spending and increased your savings, what are you doing with that extra cash? Do you have a plan to continue to spend less and save more after the virus scare subsides? According to Daco, “As long as the money is put in savings instead of being invested, then typically that tends to weigh on interest rates, it tends to curb growth and to weaken the potential of the economy.” This is why taking the extra cash and investing it is so important. Not only are you able to accumulate more wealth through investing, but you are also able to help build the economy.

Do you have an advisor that can help guide you in creating a plan to build wealth? Are there changes you want to continue to make? Do you have new financial goals? Maybe you are like me, and you have realized that you can live off of less, and now some of your dreams can come into fruition even sooner than you planned or expected just by adjusting your habits.

If you don’t currently have an advisor, or if you have an advisor and are not happy with the way they are handling your finances, reach out to us at Goodwin Investment Advisory.

We make the process simple. You can call us at (678) 741-2730 or go to our website to set up an intro call with Tara. She will listen to your story and answer any questions you might have. You will love her! The call generally lasts 15-20 minutes and is completely free. Next, we set you up with a 60-minute free consultation with one of our advisors, who will listen to you and help guide you as you discuss your personal financial goals. From there you can choose to join our client family and have access to all of our services, plus our unparalleled customer service. We are here for you.

Disclosure – All investment carries risk, and we cannot guarantee performance or results. Past performance does not guarantee future results. GIA does not earn any compensation from any of the non-GIA links provided in these resources. The market insights, podcast, blogs, book recommendations, self improvement thoughts, food recipes and activities are based on our perspectives and experience, and may not apply to your unique situation or be appropriate for your health and wellness. We are not aware of any conflicts of interest relating to any testimonials or endorsements. Please contact us for any questions relating to the content above, or to discuss how we can support you in your specific situation, and help you to reach your financial and personal goals.

Share This Story, Choose Your Platform!

Related Posts

{kind=link}

{kind=link}

{kind=link}